Introduction

Getting approved for a business loan isn’t just about needing money—it’s about proving you’re trustworthy to lenders. If you’ve faced rejection or want to make sure you get approved the first time, you’re in the right place.

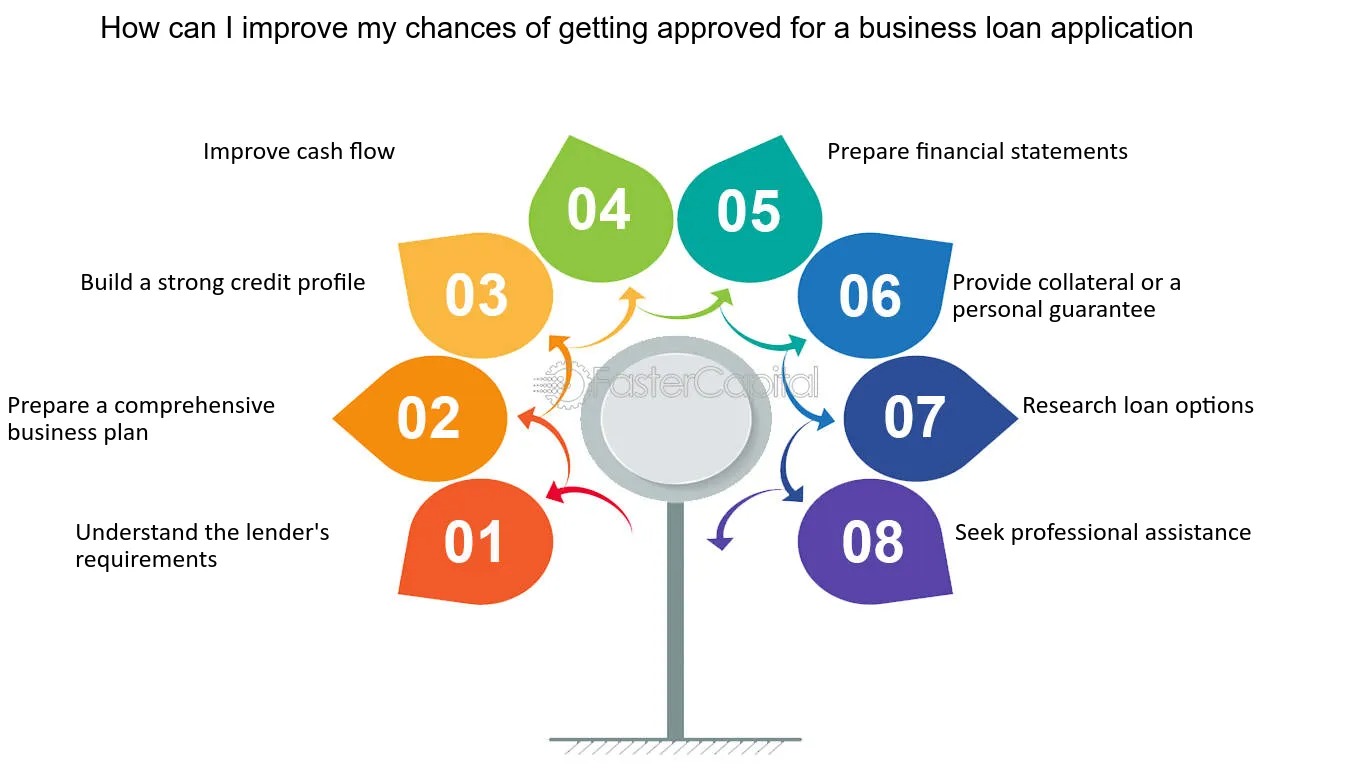

Here are 10 proven strategies to improve your chances of business loan approval in 2025.

✅ 1. Know Your Credit Scores (Business & Personal)

Lenders look at both your business and personal credit history. A poor score can mean rejection or high interest rates.

Tip:

Aim for a personal credit score of 680+ and build your business credit with vendors and small credit lines.

✅ 2. Organize Your Financial Documents

Make sure your financial records are complete, clean, and consistent.

Prepare:

- Balance sheets

- Profit and loss statements

- Tax returns (2–3 years)

- Cash flow projections

Bonus: Include a detailed business plan showing how you’ll use the loan.

✅ 3. Reduce Existing Debt

Too much current debt can make lenders think you’re overleveraged.

Tip:

Pay down credit cards or other loans where possible before applying.

✅ 4. Choose the Right Type of Loan

Don’t apply blindly. Different loans suit different business needs—term loans, lines of credit, SBA loans, etc.

Tip:

Match your loan type with your actual goal. This shows lenders that you’ve done your homework.

✅ 5. Apply to the Right Lenders

Big banks aren’t your only option. Credit unions, online lenders, and alternative funding sources may have more flexible requirements.

Tip:

Research lenders who specialize in your industry or loan size.

✅ 6. Have a Clear Use Case

Lenders want to know exactly how the funds will be used and how that will generate returns.

Example:

Don’t just say “growth.” Say, “$20,000 will be used to purchase new delivery vans expected to increase revenue by 30%.”

✅ 7. Strengthen Your Cash Flow

Cash flow is king. Lenders want to see that you can repay the loan on time.

Tip:

Avoid negative cash flow months before applying, and show consistent monthly income.

✅ 8. Offer Collateral (If Possible)

While not always required, collateral can significantly increase your approval odds and lower your rate.

Tip:

This can be equipment, inventory, vehicles, or even business receivables.

✅ 9. Get Prequalified First

Prequalification lets you check if you’re likely to get approved—without hurting your credit.

Tip:

Use prequalification tools to test the waters before making official applications.

✅ 10. Avoid Applying to Multiple Lenders at Once

Too many hard inquiries in a short period can lower your credit score and raise red flags.

Tip:

Apply strategically and space out your applications if needed.

🔗 Internal Linking Suggestions:

- Link to Article #5 (loan application mistakes)

- Link to Article #2 (low-interest business loan tips)

- Add a CTA: “Check your eligibility now – no credit impact!”

✅ Final Thoughts

Business loan approval isn’t just luck—it’s strategy. By building strong credit, cleaning up your finances, and choosing the right lender and loan type, you can dramatically increase your approval odds in 2025.

Lenders want to say “yes.” Help them feel confident that you’ll repay.